Learn how flood insurance, hazard insurance, parish differences, credit, assets, reserves, and rental income affect DSCR loan approval for New Orleans area investment properties.

New Orleans DSCR Loans in 2026: How Flood Insurance Can Make or Break Your Approval

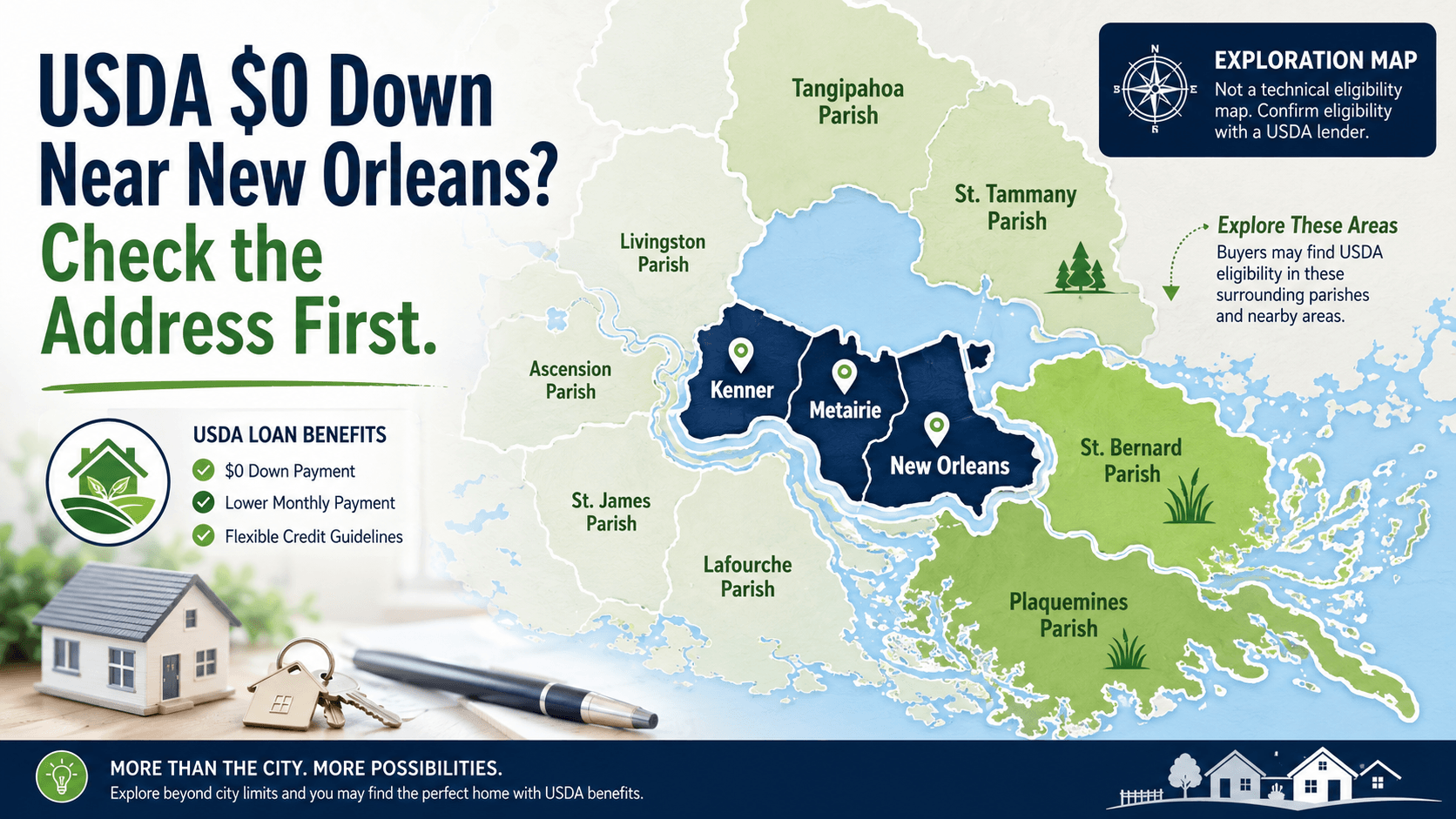

If you are buying an investment property in New Orleans, Metairie, Gretna, Kenner, Slidell, Chalmette, or anywhere across the surrounding parishes, the rent number is only part of the story.

With a DSCR loan, the property’s income helps determine whether the deal works. But in Southeast Louisiana, flood insurance, hazard insurance, taxes, HOA dues, and local rental rules can change the numbers quickly.

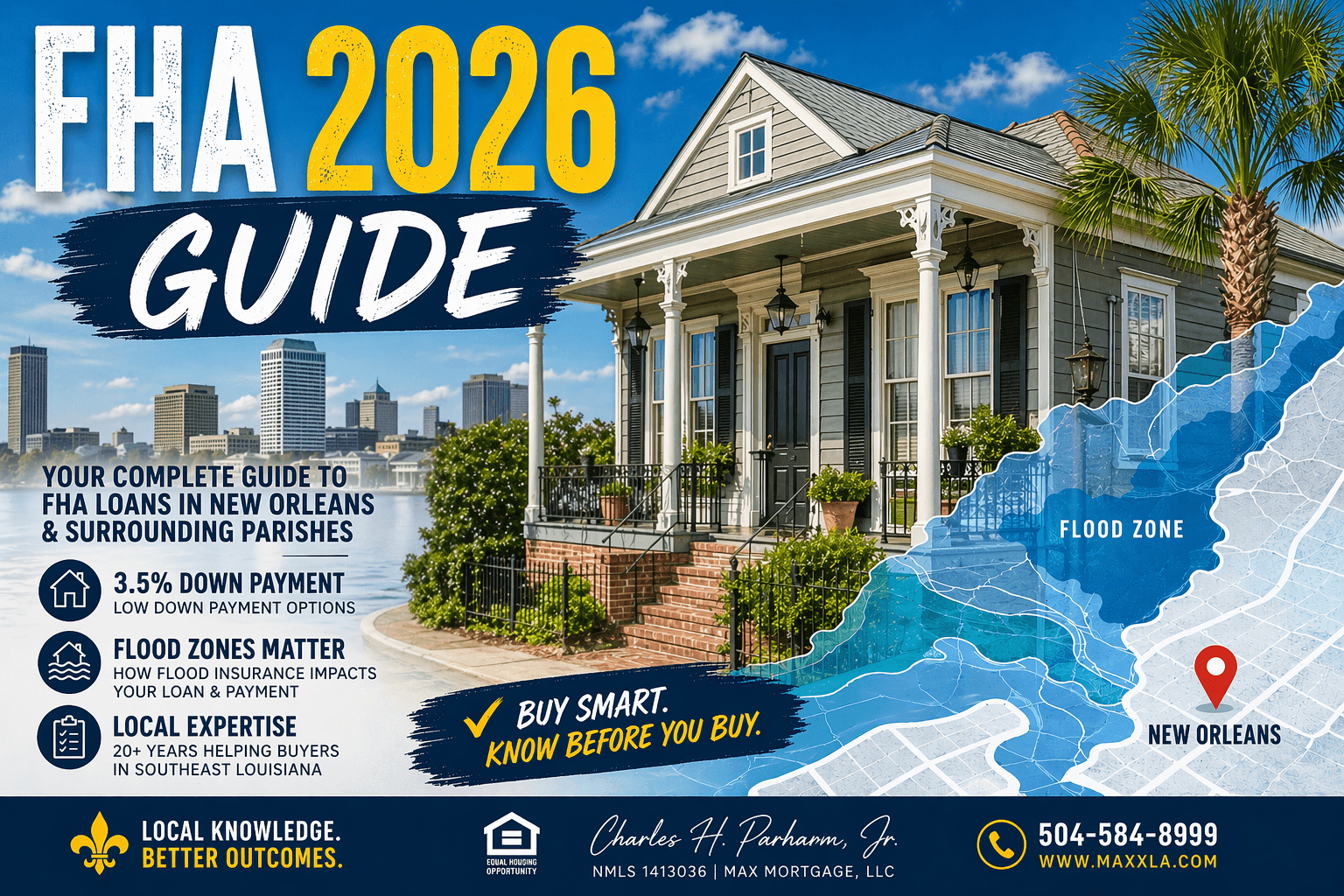

I’m Charles H. Parharm, Jr., NMLS 1413036, with Max Mortgage, LLC. After more than 20 years in the mortgage and real estate industry, I have learned that investors need more than a generic DSCR calculator. You need a local mortgage strategy that reviews credit, assets, down payment, reserves, insurance, flood risk, and whether the property can truly support itself.

At Max Mortgage, we do not usually see investors surprised by insurance late in the process because we address it upfront during the consultation. That is the goal: identify the real numbers early so the investor, Realtor, and lending team can move forward with clarity.

What Is a DSCR Loan?

A DSCR loan, or Debt Service Coverage Ratio loan, is a mortgage option commonly used by real estate investors. Instead of focusing mainly on the borrower’s personal income, the lender looks closely at whether the property’s rental income can support the monthly housing payment.

In plain English, this program can be great for investors because it generally does not require traditional income verification. If the investor has the credit, assets, and the property supports itself, the file can make sense.

The basic formula is:

DSCR = Rental Income ÷ Monthly Property Payment

That monthly property payment typically includes:

- Principal and interest

- Property taxes

- Hazard insurance

- Flood insurance when required or applicable

- HOA dues if applicable

This is why insurance matters so much in Louisiana. A property may look strong based on rent alone, but the DSCR can change once the full payment is calculated.

The Three Things We Review First on a DSCR Deal

When a Realtor or investor brings us a potential DSCR opportunity, we do not start by guessing. We start with the fundamentals.

1. Credit Score

Ideally, we like to see a credit score above 700. That does not mean every scenario below 700 is automatically impossible, but stronger credit usually gives the investor more options and can help improve the overall loan profile.

2. Assets

The investor needs enough assets for the expected down payment, closing costs, and reserves. In many DSCR scenarios, investors should be prepared for:

- 20% down payment

- Closing costs

- 3 to 6 months of reserves

This is important because DSCR loans are designed for investment properties. Lenders want to see that the investor has enough strength to handle the transaction and manage the property after closing.

3. The Property Must Support Itself

This is the heart of the DSCR loan.

Ideally, the estimated rent should be about 25% greater than the estimated mortgage payment. That means the property has a stronger chance of supporting itself instead of being too tight on cash flow.

For example, if the estimated total mortgage payment is $2,000, we would ideally like to see estimated rent around $2,500 or higher.

That gives the deal more breathing room.

Why Flood Insurance Matters So Much in New Orleans DSCR Loans

In many markets, investors focus mostly on rent, rate, price, and down payment. In the New Orleans area, flood insurance can be the difference between a deal that works comfortably and a deal that needs more review.

A rental property in Orleans Parish may have a different insurance profile than a similar property in Jefferson Parish, St. Bernard Parish, St. Tammany Parish, or Plaquemines Parish. Even two homes just a few blocks apart can have different flood risk, elevation, insurance costs, and underwriting concerns.

Local Insight

At Max Mortgage, we make it a point to account for estimated insurance upfront in the beginning of the consultation. That includes hazard insurance and flood insurance when applicable. This is one reason we do not commonly see investors blindsided by insurance late in the process.

The better approach is simple: review the full monthly payment early, then decide if the property still makes sense.

What This Means for You in the New Orleans Area

For local investors, DSCR approval is not just about whether the rent is high enough. It is about whether the rent is high enough after the full Louisiana cost structure is included.

For example, let’s say an investor is looking at a rental property in the New Orleans area.

Estimated monthly rent: $2,500

Estimated principal and interest: $1,650

Taxes: $300

Hazard insurance: $350

Flood insurance: $250

Total estimated monthly payment: $2,550

In that example, the property may not support itself the way we would like. But if the insurance is lower, rent is higher, the down payment changes, or the purchase price is negotiated, the deal may look different.

That is why DSCR planning should happen before the offer is final, not after.

Orleans Parish vs. Jefferson Parish DSCR Math

Orleans Parish, Jefferson Parish, St. Tammany Parish, St. Bernard Parish, and surrounding areas all have their own local realities.

An investor buying in New Orleans may be looking at double-shotgun rentals, small multifamily properties, or short-term rental possibilities. An investor buying in Metairie, Kenner, Gretna, Harvey, or Marrero may be comparing different insurance and flood-risk factors. On the Northshore, areas like Slidell, Mandeville, and Covington may bring a different mix of property taxes, insurance, rents, and flood considerations.

The lesson is simple: do not assume one parish’s numbers apply to another parish.

People Also Ask: DSCR Loan Questions Investors Are Searching

What DSCR ratio do I need to qualify?

Many DSCR loan programs prefer to see the rental income cover the property payment. At Max Mortgage, we like to see estimated rents that are approximately 25% greater than the estimated mortgage payment when possible. That stronger cushion can help the property show that it supports itself.

Does flood insurance count in the DSCR calculation?

Yes, if flood insurance is part of the property’s required or actual housing expense, it can affect the total monthly payment used in the DSCR calculation. That is why we account for estimated insurance upfront during the consultation.

Can I use Airbnb or short-term rental income for a DSCR loan?

Possibly, depending on the lender, property, documentation, and local rules. In New Orleans especially, short-term rental rules and permit status matter. You do not want to assume Airbnb income will be accepted without checking the guidelines first.

Are DSCR loans only for experienced investors?

No. DSCR loans can be used by new and experienced investors. However, the investor still needs to be prepared with credit, assets, down payment, reserves, and a property that supports itself.

Can I close a DSCR loan in an LLC?

Many DSCR programs allow the loan to close in an LLC, but requirements vary. Investors should review this early, especially if they are building a portfolio or buying property for business purposes.

Myth-Busting: Common DSCR Mistakes in New Orleans

Myth 1: If the rent is high, the deal automatically works.

Not always. Rent is only one side of the equation. Insurance, taxes, HOA dues, flood coverage, and the loan payment all affect the DSCR.

Myth 2: DSCR loans mean there are no rules.

DSCR loans may not require traditional income verification, but that does not mean the file is not reviewed carefully. Credit, assets, reserves, property condition, rent, and loan structure still matter.

Myth 3: Every lender calculates DSCR the same way.

Not true. Guidelines can vary by lender. Some may treat short-term rental income differently. Some may have different reserve requirements, credit score requirements, or DSCR thresholds.

Myth 4: A generic online calculator is enough.

A calculator can help you start, but it does not replace a real loan review. Local insurance, taxes, rents, property type, and parish-specific issues can change the outcome.

DSCR Loan Checklist for New Orleans Area Investors

Before you write an offer, gather:

- Property address

- Estimated purchase price

- Estimated monthly rent

- Estimated property taxes

- Hazard insurance estimate

- Flood insurance estimate

- HOA dues if applicable

- Credit score range

- Available down payment

- Estimated closing cost funds

- 3 to 6 months of reserves

- LLC information if applicable

- Short-term rental permit details if using STR income

This gives your mortgage team a much clearer picture of whether the deal may work.

Action Plan: How to Review a DSCR Deal Locally

Step 1: Review credit first

Ideally, your credit score should be above 700. Stronger credit may give you better options and a cleaner path through the process.

Step 2: Confirm your available assets

Make sure you have enough for the down payment, closing costs, and reserves. For many investors, that means planning for 20% down plus 3 to 6 months of reserves.

Step 3: Get realistic rent numbers

Do not use wishful rent. Use realistic market rent, lease income, or acceptable rental support.

Step 4: Get insurance numbers early

Do not wait until late in the process to estimate hazard and flood insurance. In Louisiana, insurance can change the deal.

Step 5: Make sure the property supports itself

The goal is for the estimated rent to be strong enough to cover the payment with room to spare. Ideally, we like to see rent about 25% greater than the estimated mortgage payment.

Step 6: Review the full DSCR picture with a local mortgage professional

This is where local experience matters. A deal that looks weak at first may have options, and a deal that looks strong online may need a second look.

FAQ: New Orleans DSCR Loans and Flood Insurance

1. Can flood insurance cause a DSCR loan issue?

Yes, it can affect the numbers. If the total payment becomes too high compared to the rental income, the DSCR may not meet the lender’s requirement. That is why we estimate insurance upfront.

2. Are DSCR loans available for New Orleans multifamily properties?

Yes, DSCR loans may be available for certain investment properties, including small multifamily properties, depending on the program and property details.

3. Do DSCR loans require personal income documentation?

Many DSCR programs do not require traditional income verification. The focus is often on credit, assets, reserves, and whether the property supports itself.

4. Can I use a DSCR loan for a short-term rental in New Orleans?

Possibly. However, New Orleans short-term rental rules can be specific. Permit status and acceptable income documentation should be reviewed early.

5. Is Jefferson Parish easier than Orleans Parish for DSCR loans?

Not automatically. Each property must be reviewed individually. Insurance, taxes, rent, flood risk, property condition, and loan structure all matter.

6. What is the biggest thing investors should prepare for?

Investors should prepare for credit review, 20% down payment in many cases, closing costs, 3 to 6 months of reserves, and a property that can support itself.

7. Should Realtors send investor deals early?

Yes. The earlier we review the property address, rent estimate, insurance estimate, and buyer profile, the better we can help determine whether the numbers may work.