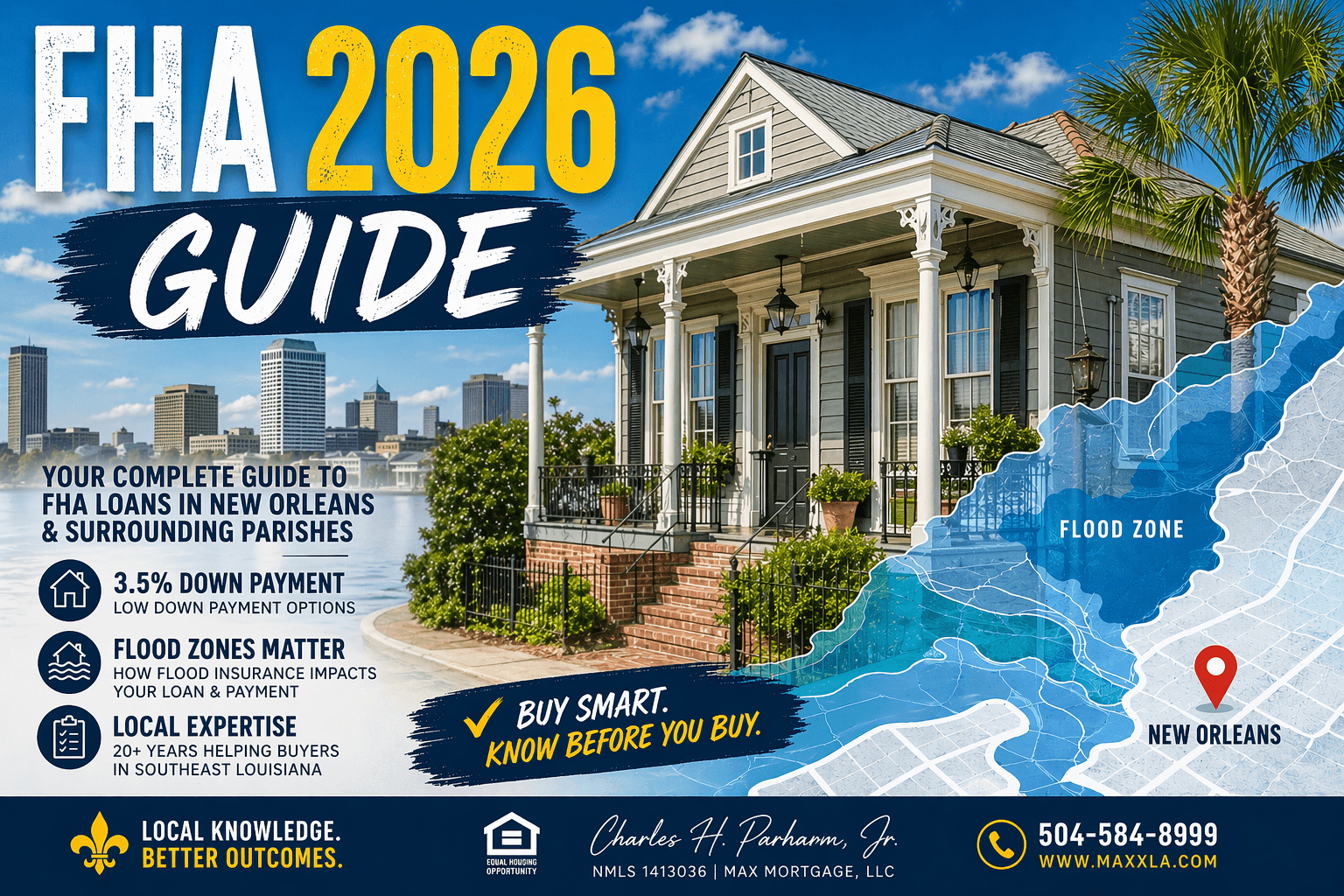

Thinking about an FHA loan in New Orleans? Learn how credit, insurance costs, flood zones, and approval rules affect your home purchase in 2026.

FHA Loans in New Orleans (2026): What Buyers Must Know Before Getting Approved

The Truth About FHA Loans in Today’s New Orleans Market

If you’re thinking about buying a home in the New Orleans area, you’ve probably heard that FHA loans are one of the easiest ways to get started.

That’s true… but only part of the story.

In today’s market, it’s not just about your credit score or down payment. It’s about how everything comes together, including insurance costs, flood zones, property condition, and your total monthly payment.

After more than 20 years in the mortgage industry here in Southeast Louisiana, I can tell you this:

The buyers who win are the ones who understand how FHA really works in our local market.

Let’s break it down.

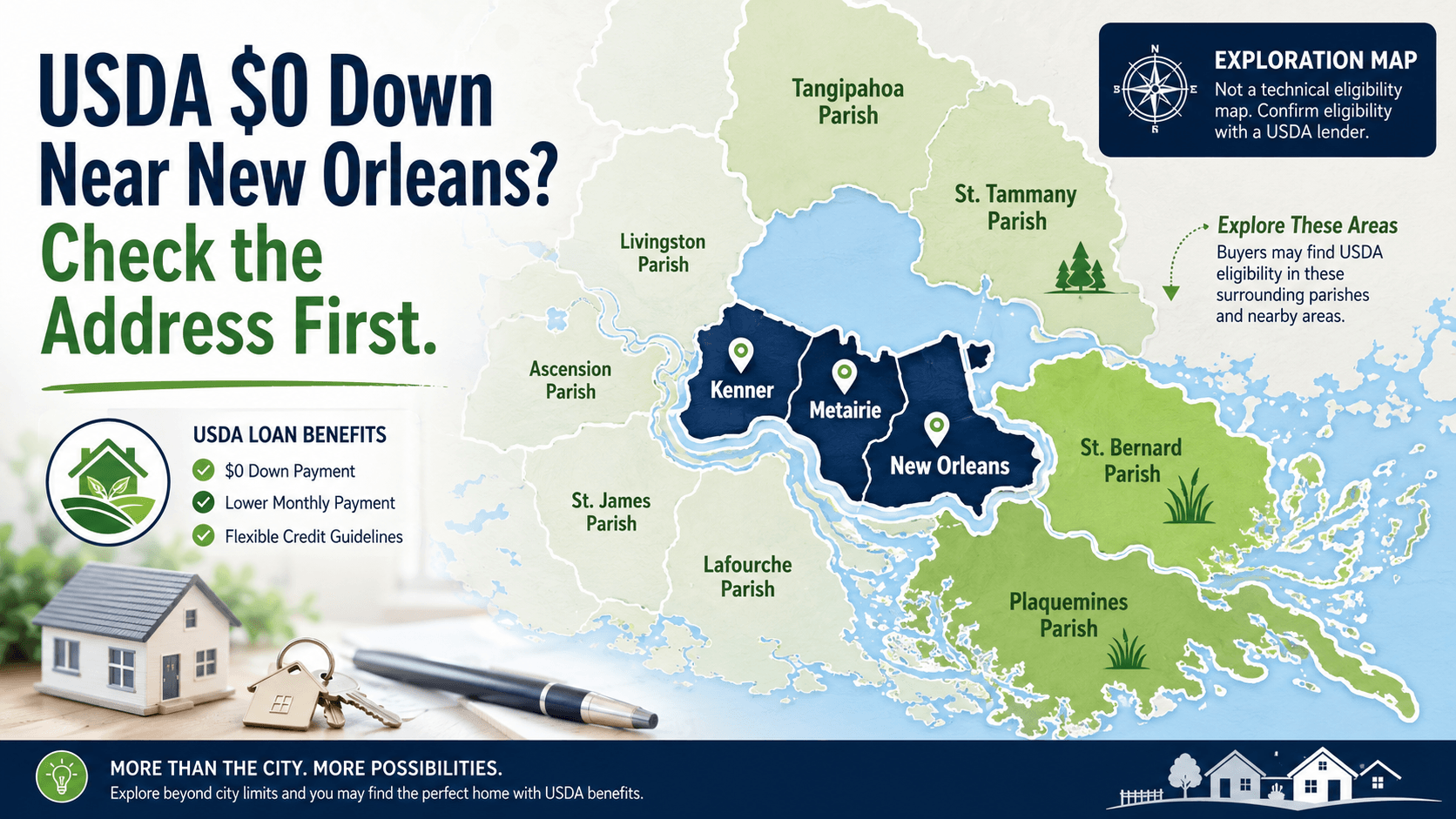

What Makes FHA Loans So Popular in New Orleans?

FHA loans are designed to help buyers who may not qualify for conventional financing.

Here’s why they’re so widely used across Orleans Parish, Jefferson Parish, St. Bernard, and St. Tammany:

Lower credit score flexibility (as low as 580 in many cases)

Down payment as low as 3.5%

More forgiving on past credit events

Allows higher debt-to-income ratios than conventional loans

For many first-time homebuyers, FHA is the entry point into homeownership.

The Real Challenge in 2026: It’s Not Just the Loan

Local Insight

In the New Orleans market, one of the biggest factors affecting FHA approvals right now is not the loan guidelines.

It’s insurance and total payment.

Between homeowners insurance, flood insurance, and property taxes, your monthly payment can vary dramatically depending on location.

That means two homes at the same price can have completely different affordability levels.

How Insurance and Flood Zones Impact FHA Approval

This is where many buyers get caught off guard.

Key factors lenders must consider:

Homeowners insurance cost

Flood insurance requirement (especially in FEMA flood zones)

Property elevation and risk classification

Total monthly payment vs your income

Example:

A $250,000 home in a lower-risk flood zone may have:

Lower insurance

Lower total monthly payment

Easier FHA approval

The same-priced home in a higher-risk zone could:

Increase your payment significantly

Push your debt ratio too high

Potentially disqualify you

FHA Credit Requirements (What Actually Matters)

Yes, FHA is known for flexible credit, but here’s what really matters:

Minimum 580 score for 3.5% down (general guideline)

620+ often gives you stronger approval options

Payment history matters more than score alone

Recent late payments can impact approval

Lenders are looking at your full financial picture, not just a number.

FHA Property Requirements in Louisiana

FHA loans also have property standards that must be met.

Common issues we see locally:

Roof condition

Electrical or plumbing concerns

Termite damage (very common in Louisiana)

Peeling paint (especially in older homes)

If the property does not meet FHA standards, repairs may be required before closing.

What This Means for You in the New Orleans Area

If you’re buying in this market, here’s what you need to understand:

Your approval is based on total monthly payment, not just price

Insurance and flood zones play a major role

Not every home will qualify for FHA financing

Pre-approval needs to be done strategically, not just quickly

This is why working with someone who understands the local market matters.

FHA vs Conventional in New Orleans (Quick Comparison)

Feature FHA Loan Conventional Loan

Credit Flexibility More flexible More strict

Down Payment 3.5% minimum 3% to 5% typical

Insurance Required (MIP) Can be removed

Property Standards Stricter More flexible

For many buyers, FHA is the best starting point. But it is not always the best long-term option.

People Also Ask (Answered)

Can I get an FHA loan with bad credit in Louisiana?

Yes, FHA allows lower credit scores, but your overall financial profile still matters.

Do FHA loans require flood insurance in New Orleans?

If the property is in a designated flood zone, flood insurance is required.

What is the minimum down payment for FHA?

Typically 3.5% of the purchase price.

Are FHA loans only for first-time buyers?

No. You can use FHA more than once under certain conditions.

How long does it take to close an FHA loan?

Most FHA loans can close in around 3 to 4 weeks with the right structure.

Common FHA Myths (Debunked)

Myth 1: FHA is only for low-income buyers

Truth: FHA is for buyers who need flexibility, not just low income.

Myth 2: FHA homes are “harder to buy”

Truth: The key is choosing the right property upfront.

Myth 3: FHA always costs more long-term

Truth: It depends on your strategy. Many buyers refinance later.

Action Plan for FHA Buyers in New Orleans

If you’re thinking about using an FHA loan, here’s your next move:

Step 1: Get a real pre-approval

Not just a quick number. A full breakdown including insurance and taxes.

Step 2: Understand your monthly payment range

Focus on comfort, not just qualification.

Step 3: Target the right properties

Avoid homes that may fail FHA appraisal.

Step 4: Work with experienced professionals

Loan structure and local knowledge matter.

FAQ: FHA Loans in Louisiana

- What credit score do I need for FHA in Louisiana?

Typically 580+, but stronger approvals often come with higher scores. - Can I buy a multi-family property with FHA?

Yes, up to 4 units if you live in one of them. - Are closing costs high with FHA?

They can be similar to other loan types, but seller concessions may help. - Can I refinance an FHA loan later?

Yes, many buyers refinance into conventional loans later. - Does FHA allow down payment assistance?

Yes, many programs can be combined with FHA.

Let’s Talk Strategy

Every situation is different, especially in a market like New Orleans where insurance, flood zones, and property conditions all play a role.

The goal is not just to get approved.

The goal is to set you up to win.