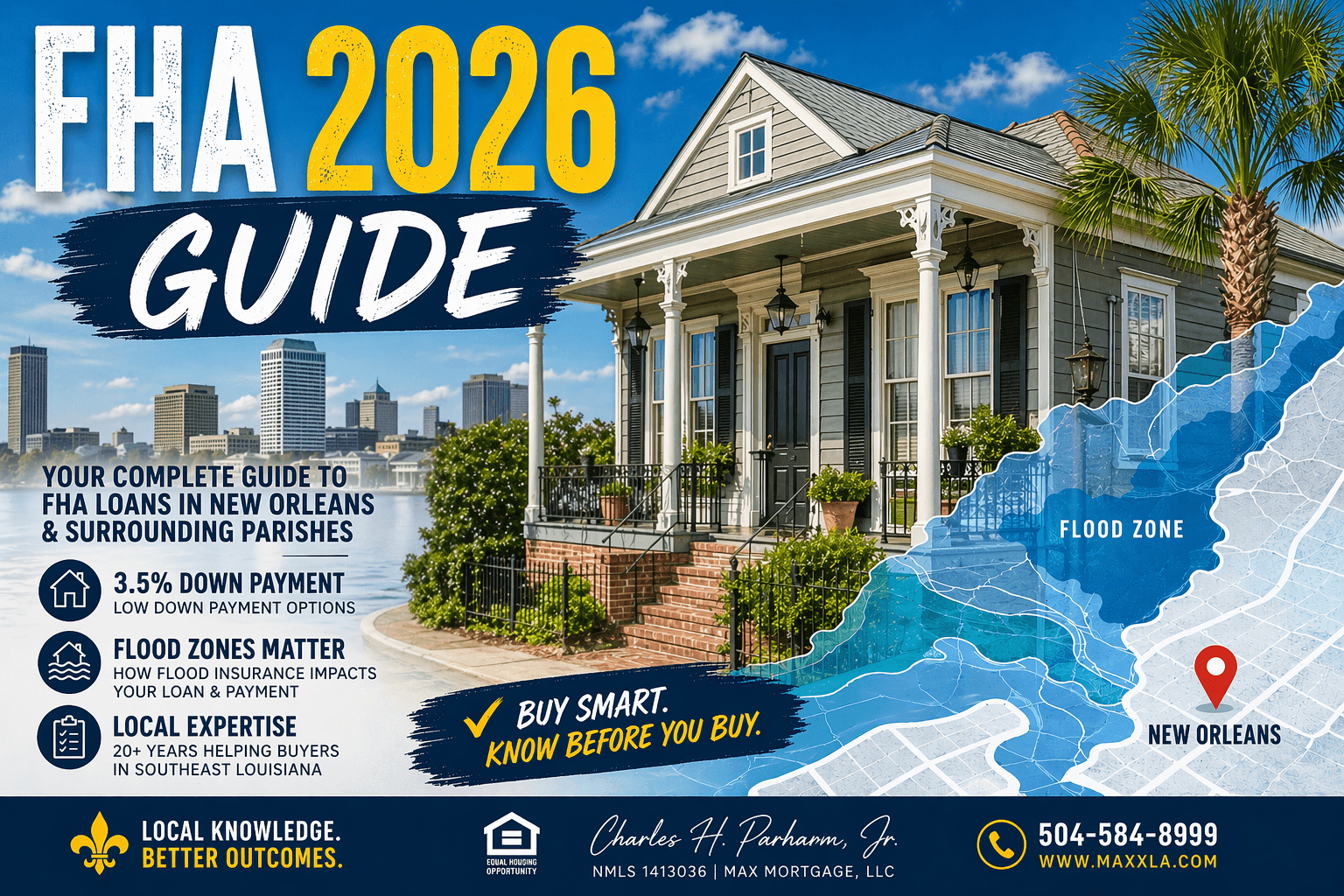

Buying with FHA in New Orleans? Learn 2026 loan limits, local assistance programs, insurance costs, and how to determine your real monthly payment.

New Orleans FHA First-Time Homebuyer Guide for 2026

Loan Limits, Down Payment Help, and the Real Monthly Payment

Buying your first home in the New Orleans area can be exciting. But for many first-time buyers, it can also feel overwhelming.

You might be asking questions like:

- How much house can I afford?

- How much money do I need down?

- Can I use down payment assistance?

- Why does the payment online look different from what lenders tell me?

For many buyers across the New Orleans metro area, the answer often involves an FHA loan.

FHA loans remain one of the most popular mortgage programs for first-time buyers because they offer:

- lower down payments

- flexible credit guidelines

- the ability to combine with certain assistance programs

However, buyers in Southeast Louisiana face an additional factor that can significantly affect affordability:

insurance and escrow costs.

Understanding how these costs affect your real monthly payment is critical before you start house hunting.

With more than 20 years helping homebuyers navigate the mortgage process, I often explain the process using something I call the Affordability Stack.

The FHA Affordability Stack

When determining what a buyer can realistically afford, three layers must be considered.

Layer 1: FHA Loan Limits

Each year the U.S. Department of Housing and Urban Development establishes maximum FHA loan amounts.

For most Louisiana markets, including the New Orleans metro area, the 2026 FHA loan limit for a single-family home is approximately $541,287.

This number represents the maximum loan amount, not necessarily what a borrower will qualify for.

Your qualification depends on:

- income

- debts

- credit profile

- total monthly payment including insurance and taxes

Layer 2: Down Payment and Closing Cost Assistance

Saving for a down payment is often the biggest obstacle for first-time buyers.

Fortunately, some programs may help eligible buyers reduce upfront costs.

Examples include programs offered through:

- the City of New Orleans

- Finance New Orleans

- Louisiana Housing Corporation

Some assistance programs may offer:

- forgivable second mortgages

- soft second loans

- closing cost grants

- deferred payment assistance

Eligibility varies depending on:

- income limits

- purchase price limits

- homebuyer education requirements

- first-time buyer status

A knowledgeable mortgage advisor can help determine which programs may apply to your situation.

Layer 3: The Real Monthly Payment

This is where many buyers are surprised.

Your monthly mortgage payment typically includes:

- principal

- interest

- property taxes

- homeowner’s insurance

- possibly flood insurance

In the New Orleans region, insurance costs can represent a meaningful portion of the total payment.

This means two homes with identical prices can produce very different monthly payments depending on location.

Local Insight from Charles Parharm, Jr.

One of the most common mistakes first-time buyers make is shopping for homes before getting pre-approved.

According to Charles Parharm, Jr., Mortgage Loan Advisor and NAMB Certified FHA Mortgage Professional:

“The most common mistake I see FHA first-time buyers make is they want to go look at houses before they have been pre-approved. Before anyone goes to look at houses, they should submit an application and get pre-approved so they know what their purchasing power is. When a homebuyer is pre-approved, it also lets the seller know they are serious about purchasing a home.”

Pre-approval not only clarifies buying power, it also strengthens a buyer’s position when submitting an offer.

Why FHA Is So Popular for First-Time Buyers

In Charles’s experience working with first-time homebuyers in the New Orleans area:

“Approximately 90% of my first-time buyers purchase their home using FHA financing.”

This popularity largely comes from FHA’s flexible qualification guidelines.

Compared to some other loan types, FHA often allows buyers to qualify with:

- lower credit scores

- smaller down payments

- higher allowable debt ratios

This flexibility makes FHA an important pathway to homeownership for many buyers.

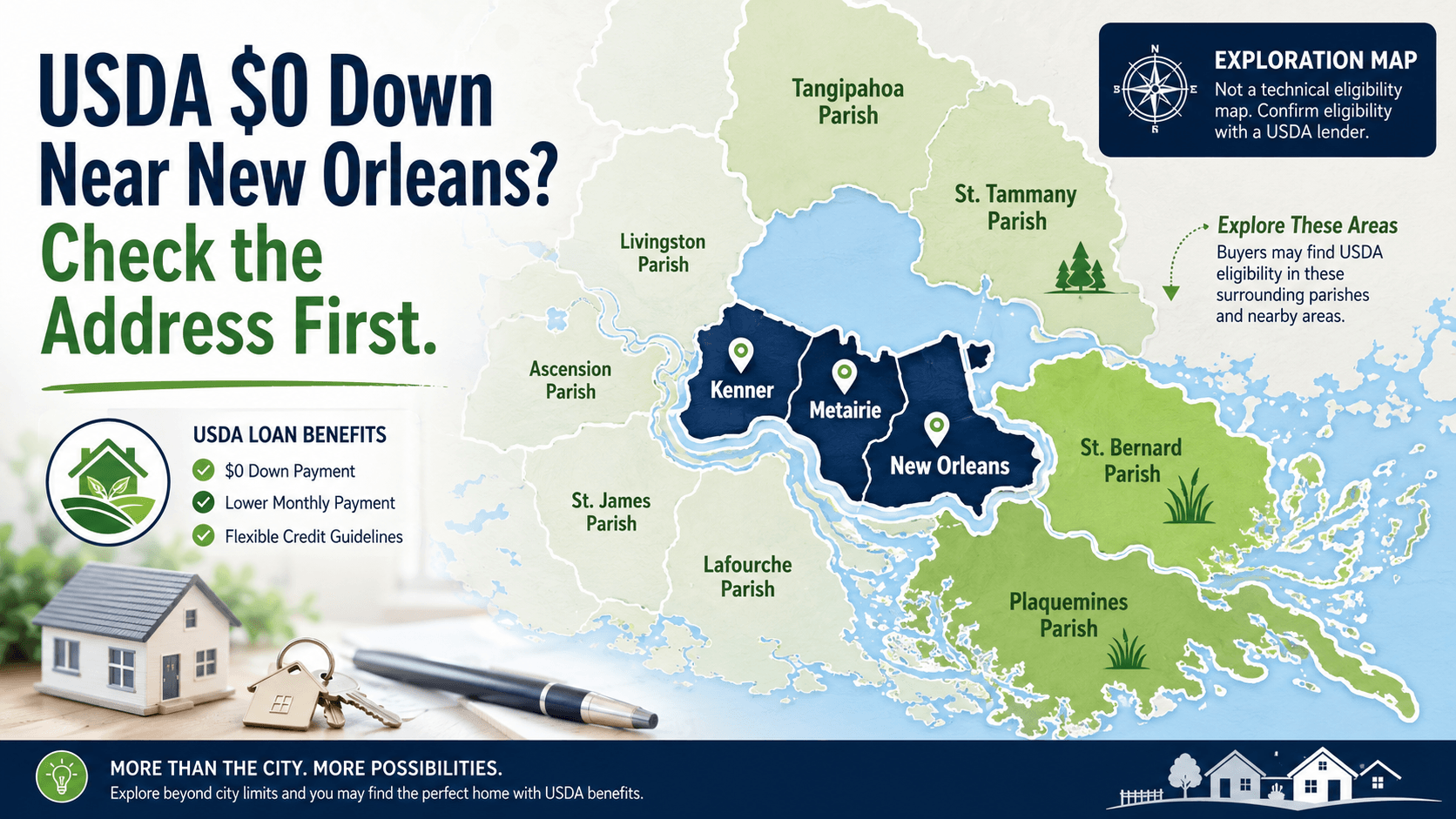

What This Means for Buyers in the New Orleans Area

When purchasing a home in Southeast Louisiana, your monthly payment can vary significantly based on location.

Factors that can affect affordability include:

- flood zone designation

- insurance carrier pricing

- property taxes by parish

- home condition and age

For example, homes across:

- Orleans Parish

- Jefferson Parish

- St. Tammany Parish

- St. Bernard Parish

may have different insurance and tax structures that impact the final mortgage payment.

Real Example: How Insurance Can Affect Loan Approval

Insurance costs can vary widely between insurance providers.

Charles recently helped a buyer navigate exactly this situation.

“One of my recent homebuyers had an insurance quote from one agency that pushed his debt ratios slightly above qualifying. We were able to obtain another insurance quote that was less expensive, and that allowed him to qualify for the home purchase.”

This example highlights why reviewing insurance options early in the process can be important.

People Also Ask

What is the minimum down payment for FHA?

Many FHA loans allow a down payment as low as 3.5% depending on credit qualifications.

What credit score do you need for FHA?

Credit requirements vary depending on the lender and borrower profile.

Can FHA loans be used with down payment assistance?

Yes, many assistance programs may be used with FHA financing if eligibility requirements are met.

Is flood insurance required for FHA loans?

Flood insurance may be required if the property is located in certain designated flood zones.

Are FHA loans only for first-time buyers?

No. FHA loans are commonly used by first-time buyers but are not limited to them.

Myth Busting: FHA Loan Misconceptions

Myth: FHA loans are only for buyers with poor credit

Reality: Many buyers with good credit choose FHA because of its low down payment requirement.

Myth: FHA homes must be newly renovated

Reality: FHA homes must meet minimum property standards but do not have to be new.

Myth: Online payment estimates are accurate

Reality: In Louisiana, insurance and tax estimates can significantly change a buyer’s final payment.

Action Plan for First-Time Buyers

If you are thinking about purchasing a home with FHA financing, here is a smart starting strategy.

Step 1

Review your income, debts, and monthly budget.

Step 2

Submit a mortgage application to determine purchasing power.

Step 3

Explore potential down payment assistance programs.

Step 4

Estimate insurance and tax costs before making offers.

Step 5

Work with a knowledgeable mortgage advisor who understands the local market.

Charles emphasizes the importance of professional guidance early in the process:

“The best advice I can give a first-time homebuyer is to review their budget and circumstances, then speak with a qualified mortgage loan advisor who can explore the programs that fit their goals and needs.”

FAQ: FHA Loans in the New Orleans Area

How much money do I need to buy a home with FHA in New Orleans?

The required amount depends on the purchase price, insurance costs, and whether assistance programs are used.

Can FHA loans be used anywhere in Louisiana?

Yes. FHA financing is available throughout the state.

Can I buy a duplex with FHA?

FHA allows certain multi-unit properties if the buyer occupies one unit.

Are FHA loans easier to qualify for?

FHA loans are generally more flexible than many conventional loan options.

How long does FHA loan approval take?

Timelines vary depending on documentation, underwriting, and appraisal requirements.